On early November, the Ministry of Finance of Azerbaijan published the budget proposal for the year 2022. In this post, I am going to look at the document and share my opinion.

REVENUES OF THE BUDGET

When preparing the 2022 budget, the average price of oil is taken at 50 USD per barrel, which in my opinion, is a sufficiently conservative and appropriate approach. With that, the revenue of the budget in 2022 is proposed to be at 26.8 billion AZN (15.8 billion USD), which is 5.5% more than the same indicator of the 2021 budget. The main drivers behind the increase are Value Added Tax (VAT), Corporate Tax, Transfers from SOFAZ, Income Tax, Excise Tax, Custom Duties, and State Duties.

VAT revenues are expected hike by 12%[1] (or 568 million AZN) from the previous year, particularly fueled by those collected from the internal market. The major contributing factors are the extra taxes to be collected from oil sector due to rising price of oil in the global markets, as well as 8.7% forecasted expansion in non-oil sector in the upcoming year (growth of non-oil sector will be chiefly driven by tourism sector in 2022, which according to the state budget proposal is going to have a huge 48.2% growth). We also need to mention that some economic activities (notably construction of buildings) are no longer eligible for simplified tax, meaning that starting from the next year, they will have to pay VAT and income/corporate taxes

Corporate Taxes are going up by 25% (526 million AZN) in 2022. According to the Ministry of Finance, the expected high growth rate of the non-oil sector, continued reforms aimed at transparency, waning effects of the coronavirus pandemic, as well as the shift of some companies from simplified tax are the reasons behind the surge.

Excise taxes are envisioned to increase by 20% in 2022. Interestingly, similar to the budget of the last year, excise taxes collected from custom authorities will be reduced again, thus the overall rise is going to be carried by domestic production and consumption. The Ministry of Finance explains that the increase from the non-oil sector is going to be supported by higher production of goods subject to excise taxes, as well the higher rate of (as of November 2021) excise taxes levied on cigarettes. One point to note here is that there is no specific explanation for the growing excise taxes to be collected from oil products (which includes sale of fuel, cigarettes, alcoholic beverages and etc., in the domestic market). It leads me to speculate that we can expect further price hikes during the year of 2022.

The upturn in custom duties is explained by larger volume of imports in 2022. State duties are also rising since the government heightened the price of certain services such as issuing of passports, getting new biometric ID cards, registering a marriage and so on.

On the other hand, when compared to the expected revenues of 2021 (in contrast to 2021 budget legislation), the revenues of the budget in 2022 are in fact set to decline by 0.6%. That is because, some sources of revenue that contributed significantly to the budget in 2021 is no longer present in 2022, such as profit from the central bank and transfers from the guarantee fund[2]. Additionally, dividends received from the State-Owned Enterprises (SOEs) is also going to shrink by 37%. The biggest contributing SOE is the International Bank of Azerbaijan (ABB), which is going to account for 71% of the total dividends to be received in 2021. Chamber of Accounts mentions that the dividends received from large state companies are going to slump by 9.2 times in 2022. Out of the five companies that usually contribute to this amount (SOCAR, Azerbaijan Railways, Azerishiq (electricity provider), Azerbaijan Caspian Shipping Company, and Azerenerji) only one of them – Azerbaijan Caspian Shipping Company is going to pay dividends to the budget. This is an odd news, and I can’t seem to find an adequate explanation for it, especially considering the recent “trend” of making SOEs less reliant on state budget and improving their performance and transparency.

Below is a table showing the most changed revenues sources in 2022 compared to 2021.

Table 1: Change in main revenue sources in 2022.

Source: Ministry of Finance

EXPENDITURES OF THE BUDGET

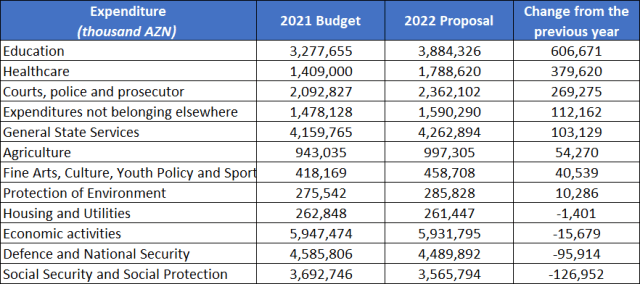

The spending side of the budget is scheduled to expand by 4.7% in 2022. When compared to the average growth rate of the post-devaluation period, which is 8.6%, the growth in this year’s budget seems more fiscally responsible. Furthermore, the major components behind the growing expenditures are education, healthcare, police force, and general state activities. Worthy to note here is that fixed capital investments, which were the traditional factor behind Azerbaijan’s increasingly expansionary fiscal policy, is actually going to decline by 2% (in the post-devaluation period, this happened only once on 2020, presumably due to the war) while the allocated funds for the newly liberated territories have remained unchanged at 2.2 billion AZN.

Education expenditures in 2022 are going up by 19%, from their previous 3.3 billion to 3.9 billion AZN. Almost half of that increment belongs to the subcategory “middle school” while the other half is distributed among other subcategories of education. Education is also selected (for the second year now) as the “pilot” category for the Medium-Term Expenditure Framework (MTEF), hence the benefits of these expenses will be judged against their costs.

Fund dedicated towards healthcare services are going to experience a hefty surge of 29%, reaching 1.8 billion AZN. The Ministry of Finance explains that the additional funding will primarily go to the mandatory insurance system, continued efforts against coronavirus, and the vaccination process.

The boost in spendings towards police force, border guard and some other relevant categories are likely a result of the efforts to re-organize the newly liberated territories of Azerbaijan.

On the other hand, the Ministry explains that the downturn in Social Security and Social Protection expenditures is a result of higher revenues of the Social Protection Fund due to relevant reforms in the sector. It is mentioned that despite lower levels of funding from the state budget, the Social Protection Fund’s expenses are set to increase by 3% next year.

Table 2: Change in expenditures in 2022.

Source: Ministry of Finance

STATE OIL FUND & BUDGET DEFICIT

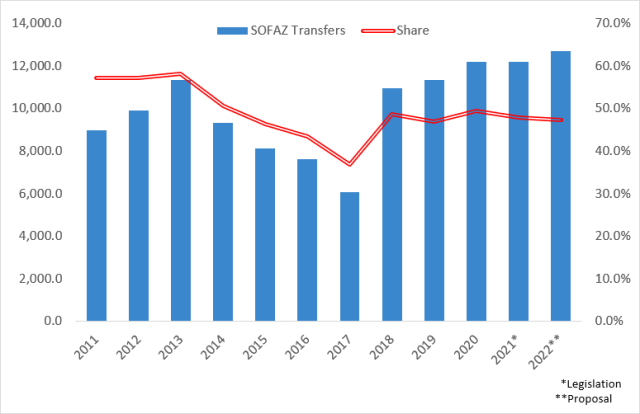

Transfers from SOFAZ are going to be 12.7 billion AZN in 2022, 500 million AZN more than transfers in 2021 and 2020. Although the Fund is expected to run a 2.17 billion AZN deficit in the base scenario, it is feasible that by the end of the next year the executed budget will have surplus, thanks to estimated price of oil being substantially above than the base scenario price of 50 USD per barrel. In fact, the Ministry has calculated that the Fund will have a balanced budget if the average price of oil reaches 55 USD in 2022.

In the state budget document, the Ministry of Finance rightfully recognizes that fiscal threat. It is calculated that a 5 USD decrease in average price of oil (from 50 USD) per barrel results in 1.4 billion AZN (or 1.86%) reduction of State Oil Fund’s assets.

Graph 1: Timeline of transfers from SOFAZ and its share in budget revenues

Source: Ministry of Finance

At the end, the deficit of the state budget 2022 will be 3,063 million AZN, which is 53 million less than the same indicator of 2021 (do note that the deficit of the executed budget in 2021 is expected to be almost 2 times lower than the legislation, hence the deficit is actually going to grow). The deficit will constitute 3.5% of GDP next year.

The main sources of financing for the budget deficit are going to be the surplus from the previous year and state debt. The large surplus (1,256 million AZN) primarily rises because the revenues collected from taxes and customs in 2021 will be quite bigger than the budget legislation initially envisioned. The Ministry also mentions that state debt will be more utilized in mid to long-term period to cover the budget deficit. It explains that this strategy principally aims at developing the internal financing market, as well as safeguarding assets of the State Oil Fund. For the budget of 2022, 1,693 million AZN of the deficit is to be financed by internal and external debt.

MY THOUGHTS AND CONCERNS

The 2022 budget project includes some positive and some negative things to note. I will first start with the good news.

- Unlike the previous years, the average price of oil has been taken at quite a conservative level. For example, last year the average price was 40 USD per barrel in budget legislation when EIA forecasts were at 49 USD. This year, the difference is far larger, as EIA estimates average price of 72 USD per barrel while the state budget takes it at 50 USD. The conservative approach is more appropriate in our case, as it allows the State Oil Fund to accumulate assets and at least limits the magnitude of procyclicality of the fiscal policy.

- The total expenditures of the budget are rising in a more stable manner next year. The growth of expenditures in 2022 is just a little higher than the estimated inflation rate (4% estimated annual inflation vs 4.7% growth in spending). Switching to Medium Term Expenditures Framework (MTEF) in the near future will also help us extensively in this matter.

- The preeminent categories behind the expenditure growth are education and healthcare, unlike the previous years where the leading push usually came from fixed capital investments. In fact, fixed capital investments are set to decline by 2% (including the 2.2 billion AZN allocated for liberated lands), which is a much welcoming development.

- The Social Security and Protection Fund is becoming less financially dependent on the state budget next year thanks to its heightened revenues from relevant reforms carried in the sector.

- Unlike budget projects of the last year, there were at least a decent level of recognition of fiscal risks in the MTEF document released in September by Ministry of Finance. These risks were also mentioned (but in a briefer form) in budget 2022 proposal. In these documents, the Ministry outlines the adverse effects of Azerbaijan’s declining oil production and the mid-term negative outlook for oil prices. It acknowledges that the current policy is fiscally unsustainable and will lead to substantial dwindling of Oil Fund’s assets.

Now let us look at negative things.

- Foremost is of course the continued dependence on oil. Despite all the strategies and goals and talks of fiscal responsibility, transfers from State Oil Fund are still on the rise.

- The Fiscal Rule was suspended for 2020 and 2021 due to the pandemic. However, although we are now about to confirm the budget of 2022, there is still no clear information about the status and design of the new rule. The Chamber of Accounts mentions that only 1 component of the previous fiscal rule will remain in the new version, which is the ratio of non-oil deficit of the consolidated budget to the non-oil GDP. If this is the case, then the scope of the fiscal rule is going to be much more limited. I am going to dedicate a different post to this issue once we learn more about the details of the updated fiscal rule.

- As mentioned above, the state debt is going to be utilized at a higher rate in the upcoming years. Although now the ratio of state debt to GDP is at reasonable levels (21.6%), we must remember that 82% of that debt is in USD and in the case of a devaluation, it can shoot up to dangerous levels. According to my calculations, devaluation of AZN from its current rate of 1.7 (1 USD = 1.7 AZN) to 2.0 would escalate the debt to GDP ratio to 24.8%.

- Estimated inflation rate of 4% is too low and unrealistic, considering all the internal and external factors. We know that there will be noteworthy pressure from domestic sources in 2022 as the increased minimum wage and pensions will broaden production costs and shift up the aggregate demand curve. Also, the producers are still adjusting to new domestic climate, as tariff council raised price of fuel, natural gas, and electricity throughout the year 2021. Therefore, we can expect that the current trend of high inflation will be carried into 2022. It is pivotal to have a realistic inflation estimation because failure to do so can lead to almost all macroeconomic forecasts being unreliable.

- Another thing that I find worrying is that the ideas of countercyclical fiscal policy are utilized when oil prices are low (such as in the year of 2020 when we suspended the fiscal rule) but are completely overlooked when it comes to high oil price periods (such as the upcoming year). This is not a healthy practice, because if we are serious about decreasing the dependency of the economy (and the budget) on oil sector, then a countercyclical fiscal policy must be followed every year, regardless of it being dictated by a fiscal rule or not. A far better practice would have been to stick to the original plan (outlined in the document on MTEF released by the Ministry of Finance in September) where the transfer from the Oil Fund were proposed to be 11.8 billion AZN based on 45 USD per barrel scenario. Yet, only two months later the new budget projections include bigger transfers from the oil fund, higher expenditures for the budget and even a larger deficit. Considering that the oil prices rose significantly in September – October, this is a textbook example of a procyclical fiscal policy and should be avoided to the extent possible.

- The Ministry mentions that they target to reduce the ratio of non-oil budget deficit of the consolidated budget to non-oil GDP in the mid-term, but it is expected to rise in the short-term. I think it is high time for us to stop justifying short-term negative trends (and bad economic policy) by setting unbinding mid/long-term positive goals and targets that are never achieved. We must move to having concrete rules that precept both short and long-term goals. The practice of setting loose mid/long-term targets with “strategic documents” do not work, proven by the ones that were drafted in 2012 for the year 2020. It is therefore imperative for us to have a comprehensive, functional, and binding fiscal rule as soon as possible.

FOOTNOTES

[1] Bear in mind that the expected amount of VAT to be collected in 2021 is significantly higher (8.5% to be exact) than that of the initial legislation. When taken that into account, the increase of VAT revenues in 2022 comes down to 3%. That is also the case for Customs Duties.

[2] Here we are talking about the “Guarantee Fund on State Debt and Assurance”, which covers the debt of State-Owned Enterprises when they fail to meet their external financial obligations (which happens rather often in Azerbaijan).