In my latest post, I delved into the topic of Azerbaijani Manat’s grim-looking short-term future following the surging demand for foreign exchange in March and concluded that there is a substantial risk of devaluation during 2020. In this post, I am going to share a concept on how the government can at least delay this devaluation for the near future and avoid exacerbating the economic situation in the country already troubled by coronavirus epidemic…

WHAT IS THE MATTER WITH MANAT?

First, I need to give a brief depiction of how foreign exchange markets operate in Azerbaijan. Most of the revenue that Azerbaijan gets from the sale of oil firstly goes to the State Oil Fund – SOFAZ for short (I say most of the revenue because a certain portion directly goes to the state budget in the form of taxation of the State Oil Company – SOCAR). Each year, when the budget of SOFAZ is drafted, they consider how much the Fund will be transferring to the State Budget. Since the revenue of SOFAZ is denominated in US Dollars (USD) whilst the State Budget operates with Azerbaijani Manat (AZN), there arises a need to exchange those dollars into manat before forwarding them to the State Budget. For that purpose, couple of times a month, the Central Bank organizes auctions with the participation of financial companies where the foreign currencies of the Oil Fund are sold in exchange for Manat. In essence, the amount of currencies sold in those auctions can be considered as an indirect indicator of the demand for foreign currencies in Azerbaijan.

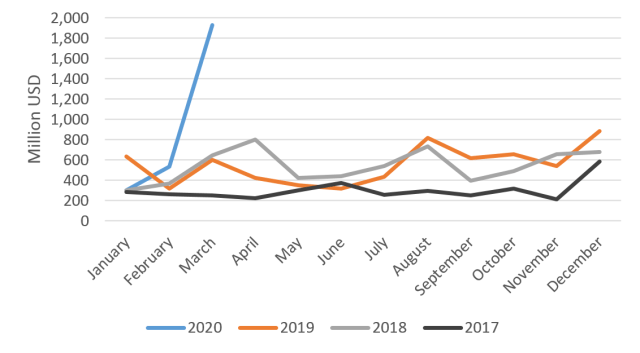

What we have observed in early 2020 was a colossal upswing in the amount of currencies sold in those auctions, as seen on the Graph 1 below.

Graph 1: Dynamics of foreign currency auctions in Azerbaijan

Source: State Oil Fund of Azerbaijan

To put it shortly, the collapse of oil prices last month persuaded people to collectively sell their Manats in exchange for other currencies, in particular the US Dollar. Faced with this wave of demand, the banks in turn stormed the auctions and bought as much currency as possible. And here is the point: the excessive demand for foreign currency is a mere result of distrust of the general populace towards the national currency. If we look at the dynamics of the previous years, we can predict that at most the demand could have been around 800 million USD in March given that there was no crash in the oil market. However, in fact it was 1,925 million USD. The additional demand of 1.1 billion USD is the corollary of the psychological trauma endured upon Azerbaijanis since the devaluations of 2015.

If this trend prevails in the upcoming months, even in a much lesser form, then devaluation of Azerbaijani Manat may be inevitable. Such a phenomenon would devastate an already fragile economy suffering from coronavirus epidemic and its side effect of historically low oil prices.

The foreign currency auctions of April may seem meager for an outside observer, but we need to recognize that it may very well be a temporary trend due to lower amounts of income of the population during the outbreak. We can, therefore, see another surge in May once the effects of epidemic start to yield. That is quite a possibility, since the quarantine is set to be coming to an end soon whilst the price of Azerbaijan’s crude oil – Azerlight is yet to suffer, mainly due to the fact that a significant portion of its demand is driven by the Aviation sector, which know lays in severe bankruptcy.

Therefore, the short-term target of the government and the Central Bank should be to postpone the devaluation as long as the epidemic and the post-epidemic recession persists. Doing that, on the other hand, is not as easy as it sounds.

SHORT TERM ESCAPE FROM DEVALUATION – GOLD COMES TO THE RESCUE

Once the expected rise in demand for foreign currencies arrive, the classic methods of calling for “calmness” and “trust in national currency” would not work, as the credibility of state officials and the Central Bank is quite dubious in the minds of Azerbaijanis. The government needs to recognize that fact and prepare alternative mechanisms to impede the devaluation if the things take unfavorable turn. In my opinion, a new and rather straightforward program by the government can, at least theoretically, withhold the devaluation: sale of gold coins to the population in exchange for the national currency.

This proposed solution may seem old-fashioned, but once we think about it more comprehensively, we see that it can settle couple of problems at the same time. Long story short, it is a good time for the population to buy gold and it is also a good time for the State Oil Fund to sell gold. This exchange between the SOFAZ and the population would also be beneficial to Azerbaijani manat. In the paragraphs below, I will try to explain the claims that I just made.

WHY WOULD PEOPLE WANT TO BUY GOLD?

I think it is clear that the reason people wish to exchange their manats into other foreign currencies is because they expect Manat to lose value and they want to preserve their wealth. Given that expectation, it does not matter what Manat is exchanged into, as long as the other side is credible enough. That is the reason why people exchange the national currency mainly into US dollars or Euros and not Turkish Liras or Russian Rubles, because the former ones have better reputation. Similar to these currencies, gold is also a trustworthy asset to hold, in mind of the population. Gold has historically proved its “safe haven” status during times of market turbulences. Especially now since the gold prices are rising steadily due to the outbreak and is anticipated to continue that upswing well into the next year[1]. Therefore, given the opportunity, the population would be more than eager to buy gold using their manats. First side of the exchange is set.

WHY WOULD SOFAZ WANT TO SELL GOLD?

As of April 2020, the Fund has 101.6 tonnes of gold in its reserves[2]. In today’s price, that gold is worth around 5.6 billion USD which is around 13.5% of total assets of the Fund. The Fund states that in accordance with the legislation, the value of its gold reserves cannot exceed the 10% of its total investment portfolio. Thus, it is also in the interest of the Fund to sale a certain portion of its gold reserves.

Not only that, the sale of gold can also help the Fund in terms of cash revenue. SOFAZ was able to provide enough foreign currencies to the market during January – March of 2020 only because they were selling the oil with the prices of December – February as part of oil futures deals. It is stated in the fund’s quarterly reports that during that period, the average price of a sold barrel of oil was 59 USD[3], far above the actual price of the last months. What that means is that the real bulk of the trouble lays still ahead for the Oil Fund of Azerbaijan and the Fund will likely be forced to convert some of its assets into cash in order to meet its responsibility of transfers to the state budget. Given the choice between selling bonds before their maturation, or stocks/real estate at the time of an economic recession, or gold when its prices have been on the rise, I think the logical choice is clear. In short, I do not see any reason why SOFAZ would be unwilling to sell a certain portion of its gold assets.

The exact amount of sale is up for discussion, of course. For example, if the Fund wishes to bring back the share of gold reserves in its total portfolio down to 10%, then it can sell approximately 1.4 billion USD worth of gold. Although in the grand scheme of things 1.4 billion USD might not look a lot, but in my opinion it would be enough to deplete the demand for foreign currencies for the time being and allow the Central Bank to delay a potential devaluation of Manat.

CONCLUSION

In conclusion, we have explored the idea of redirecting a portion of the demand for foreign currencies in Azerbaijan which stems from distrust of the population towards the national currency. A potential way to accomplish that goal could be utilizing the gold reserves of the State Oil Fund. Since the total value of gold assets are above the 10% threshold of the Fund at the moment, it would also be in its interest to sell a fraction of those assets. Additionally, such a sale can provide SOFAZ with much-needed cash at times of historically low oil prices. On the other side of the equation is the people of Azerbaijan who go to banks to exchange their manats as long as the oil prices are on the decline. The psychological trauma that have been present since devaluations of 2015 coupled with a general lack of confidence in Central Bank renders the calls of officials and similar measures inadequate. As a preventive measure, the government can offer an alternative to foreign currencies: gold coins. When one takes into account the mindset of Azerbaijani people, as well as the overall positive outlook for the gold in the near future, I believe that the population would be eager to buy gold (within their capacity, ofcourse) once it is available. When people do buy gold coins instead of US dollars or Euros, the demand for these currencies will be lowered at a certain magnitude and release some fragment of the pressure on Azerbaijani Manat. In order to ensure that these coins are accessible for most Azerbaijanis, they can be sold at ASAN service centers that cover most regions of the country. The similar experiences have been observed across the world in the past too. Last year, fearing the devaluation of Yuan, Chinese people turned to gold purchases to preserve their wealth in the context of foreign exchange controls[4].

However, please be noted that under no circumstances this measure can be taken as a medium- or long-term solution. The sale of gold, or any other assets, including crude oil should not and cannot maintain the arbitrary exchange rate of Manat forever. Sooner or later the exchange rate will have to be altered, mostly likely in a negative direction. Therefore, the most sustainable policy would be to prevent devaluation for now as long as the epidemic persists. Once everything normalizes, a swift step towards an actual floating exchange rate regime, which is long overdue since 2016, has to be taken.

FOOTNOTES

[1]https://www.cnbc.com/2020/04/21/bank-of-america-raises-gold-forecast-by-a-whopping-1000-to-3000-because-of-zero-rates.html

[2]https://www.oilfund.az/investments/gold

[3]https://www.oilfund.az/report-and-statistics/get-download-file/6_2020_1.pdf

[4]https://www.theepochtimes.com/chinese-people-are-buying-gold-taking-money-out-of-banks-and-stock-market_2989072.html