Political tensions in Turkey and sanctions against the Russian Federation resulted in sharp depreciation of Turkish Lira (TRY) and modest loss of value by Russian Ruble (RUB), creating an overall expectation of devaluation in Azerbaijan. With this post, I would like to briefly look at different factors and argue why and why not a devaluation[1] can be expected. At the end, I will give my overall conclusion on whether we should worry about Manat.

- Why Manat Might Lose Value?

There is a widely accepted idea in economics that exchange rates have an adverse relationship with exports. That is, when the currency of country A loses value against currency of country B, then the goods and services of A will become relatively cheaper, thus the country with the stronger currency (B, in this case) will face an increase in imports and decline in exports, leading to a trade deficit.

Based on that theory, I will be looking into how currencies of Azerbaijan’s main trade partners have changed in the past three months and would it have a compelling effect for our economy. Please be noted that while examining exports of Azerbaijan, I will mainly be concerned about non-oil/gas exports, since they are the ones most likely to be stirred by exchange rate fluctuations, rather than commodities such as crude oil or natural gas.

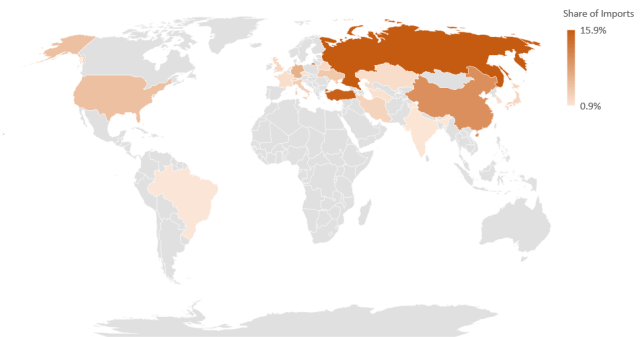

According to Center for Analysis of Economic Reforms and Communication, the top 5 destination for Azerbaijani non-oil exports during January – June period of 2018 are: Russia (319.9 million USD), Turkey (180.1 million USD), Georgia (74.1 million USD), Switzerland (69.3 million USD) and China (23.9 million USD)[2]. When it comes to imports, you may see Azerbaijan’s largest partners from the map below.

Geographic layout of Azerbaijan’s top import partners (July 2018)

Source: Customs Committee of Azerbaijan Republic

Let us now look at how Azerbaijani Manat’s (AZN) value changed against the currencies of its largest non-oil trade partners:

| Exchange Rate | 1 May, 2018 | 10 August, 2018 | Change |

| AZN/CHF | 0.583 | 0.585 | 0.2% |

| AZN/GEL | 1.441 | 1.452 | 0.8% |

| AZN/CNY | 3.723 | 4.026 | 8.1% |

| AZN/RUB | 37.037 | 39.2157 | 5.9% |

| AZN/TRY | 2.389 | 3.373 | 41.2% |

Source: Central Bank of Azerbaijan

As we can see from the table above, Azerbaijani Manat has gained value against all five of the currencies. However, the magnitude of change varies firmly. First of all, the Swiss Frank (CHF) has been roughly steady. Even if it depreciated vastly, it would be of little interest to our analysis since the bulk of Azerbaijani exports to Switzerland is consisted of a single commodity: gold. Georgian Lari also depreciated by a mere 0.8% against Manat, which is not consequential either.

Exchange rate of Chinese Yuan (CNY) on the other hand had somewhat a noteworthy downturn. However, I believe that this development is not very substantial for Azerbaijan because of two reasons: (a) Azerbaijani exports to China is not very large with only 1.81% of total non-oil/gas exports and (b) majority of products that Azerbaijan imports from China, such as telephones, computers and other electronics do not have a local substitute. Thus, the depreciation of Yuan does not possess a risk for local producers.

As mentioned before, the two most vital currencies here are of course Russian Ruble and Turkish Lira.

Russia is by far the biggest market for Azerbaijani non-oil/gas products such as fruits and vegetables. On the other hand, it is also a critical trade partner as the top exporter to Azerbaijan, since 15.88% of all imports to Azerbaijan originate from Russia[3]. Considerable part of the Russian exports to our country consists of every day consumer products such as sausages, seed oil, shampoo, soap etc. These kinds of goods are also produced locally here in Azerbaijan and face competition from Russia. On the background of a weaker Ruble, the Azerbaijani producers might have to tighten their profit margin for not losing their market share. However, since the Ruble’s depreciation is only 5.9%, it will not possess an enormous risk for the Azerbaijani economy if it stays in its current levels.

Let’s now address the elephant in the room: Turkish Lira. It has depreciated by a staggering 41.2% during the last three months against AZN. Turkey ranks second both in Azerbaijan’s import and non-oil/gas export partner. Like the imports from Russia, a certain part of Turkish products gets into competition with local manufacturers of Azerbaijan. There is no doubt that the depreciation of TRY will put fierce pressure on Azerbaijani producers who will now have to compete with almost half as cheap Turkish products in Azerbaijani market. On the other hand, when it comes to exports, not only Azerbaijani non-oil/gas products will most likely lose their grip on Turkish markets as they become expensive, they might also be squeezed out of Russian markets by Turkish competitors who also supply Russian Federation with agricultural products.

Naturally, one might wonder does Azerbaijan have any other option rather than devaluation to combat this situation? In times of strong depreciation of a trade partner, countries usually employ the policy of protectionism. Higher tariffs compensate for cheaper imports and local producers do not suffer as much. However, Azerbaijan is not likely to put protectionist measures against Russian Federation or Turkey due to strong geo-political ties. Even if it did, such a move would not address the problem altogether, as protectionist measures only “protect” against cheap imports but does nothing for lost competitiveness in exports.

Taking into account all of the above-mentioned points, we can say that depreciation of Ruble and most importantly Lira creates trouble for Azerbaijan’s foreign trade. Devaluing Manat would indeed be the most straightforward solution to the problem. However, we should also look at other factors of devaluation and why Manat should not follow such a path.

- Why Manat Might Not Lose Value?

There are several factors that tells us that the Manat should not be devalued. Particularly, stable and moderate oil prices, high dependency of financial sector on foreign currencies, and devaluation paranoia of the population. Let us look at them one by one.

As of August 11th, a barrel of BRENT Crude oil is sold for $72.81 with steady price forecasts for the upcoming years. US Energy Information Agency (EIA) forecasts that in 2019 BRENT crude oil will be sold for $70.58 per barrel[4]. Estimates of International Energy Agency (IEA)[5] and Energy Outlook of British Petroleum (BP)[6] also confirms a stable price for crude oil in the near future. Keeping in mind that 80.7% of our exports is crude oil (July 2018), as long as its price stay at its current range, Azerbaijan will receive plenty of dollars in order to keep the exchange rate of AZN. Slow increase in official foreign reserves of the Central Bank of Azerbaijan since the January of 2017 also approves that argument[7].

In my opinion, the most crucial factor that would lessen willingness of the Central Bank towards a potential devaluation is the current situation in financial sector. As of June 2018, 69.2% of all deposits[8] and 38.7% of all loans[9] by financial institutions are denominated in foreign currencies. The banks and other financial intermediaries today are almost more dependent on foreign currencies than February of 2015 when the first devaluation of Manat happened (back then the numbers were 66.9% and 40.5% respectively.) When the exchange rate of Manat was altered during 2015, the banks faced severe consequences as the devaluation doubled debt of people who took foreign currency denominated credits. Already suffering from non-performing loans, the sector started to experience colossal losses when population lost confidence in financial sector because of bank failures and withdrew deposits in vast numbers. During the last 3 years, a total of 11 banks shut down in Azerbaijan after the devaluation and confidence of population in financial intermediaries shrank immensely. Even with 100% guarantee by the government (Credit Guarantee Fund) and much higher interest rates on deposits made with Manat, a considerable portion still lacks faith in the national currency and overall the financial sector. Another devaluation surely risks even more bank failures and collapse of financial intermediaries completely. Such a phenomenon would be very tough to heal and hamper the economic growth to a great extent.

And lastly, we need to take into account the expectations of the population. As proven by the numbers given above, people do not trust the national currency. Majority understands that the current exchange rate (1 USD = 1.7 AZN) is set artificially and might change rapidly. Even if the value of Manat change from 1.7 to 1.75, people would collectively go to banks to buy dollars. There is a very nice short paper written by Rashad Hasanov of Center for Economic and Social Development (CESD) who talks about how small things (in this case, a notification by Central Bank) causes enormous panic in Azerbaijan when it comes to exchange rate[10]. Considering these, even a small devaluation would not be in the interests of the Central Bank.

Conclusion

To sum it all, I believe that the most important factor to look at is of course the Turkish Lira. Its depreciation is going to put pressure on local products in Azerbaijani markets and is likely to trouble our exporters to Turkey and Russia. Due to unlikelihood of putting higher tariffs on Turkish imports, the straightest solution for Azerbaijan would be devaluation of the national currency. On the other hand, the devaluations of 2015 were made with the order of the government because it was struggling to keep revenues and expenditures of state budget balanced. Today such a problem does not exist. It is true that contemporary circumstances decrease export potential of our non-oil sector greatly, but that is “not a binding issue.” With stable source of revenue from oil sector and positive forecasts for the upcoming years, high dependency of an already vulnerable financial sector on foreign currencies, as well as the current mindset of the population, a sizeable devaluation would be of little interest to Central Bank. In conclusion, I believe that Manat is not going to experience any significant devaluation in the upcoming months (as long as TRY doesn’t continue to lose value at its current pace). Even if Central Bank decided to pursue with devaluation, it would be a small and gradual one towards the new exchange rate of around 1 USD = 1.85 AZN or so.

Footnotes

[1] Throughout this paper I am going to use the term “devaluation” when it comes to Azerbaijan because de facto floating regime does not exist at the moment.

[2]http://iqtisadiislahat.org/store//media/documents/ixrac_icmali/2018/iyul/ExportReview2018-7.pdf

[3]http://customs.gov.az/modules/pdf/pdffolder/71/FILE_C9FAFF-4A0744-9A5FD7-65A94F-3F5341-BF6BCA.pdf

[4]https://www.eia.gov/outlooks/steo/

[5]https://www.iea.org/Textbase/npsum/oil2018MRSsum.pdf

[6]https://www.bp.com/content/dam/bp/en/corporate/pdf/energy-economics/energy-outlook/bp-energy-outlook-2018.pdf

[7]https://www.cbar.az/assets/3572/2.2.pdf

[8]https://www.cbar.az/assets/3583/2.12.pdf

[9]https://www.cbar.az/assets/3578/2.7.pdf

[10]http://cesd.az/new/wp-content/uploads/2017/10/CESD_Article_Currency_Market.pdf

A good analysis indeed,thanks fow writing this article 🙂

LikeLike

My pleasure sir, thank you for reading it

LikeLike